Ohio HB 87 Aims to Include Unborn Children as Tax Dependents

In 2019, Georgia’s legislature passed House Bill 481, known as the Living Infant Fairness and Equality (LIFE) Act. Its amendment to the state tax code allowed for the inclusion of an unborn child with a “detectable human heartbeat” as a tax dependent.

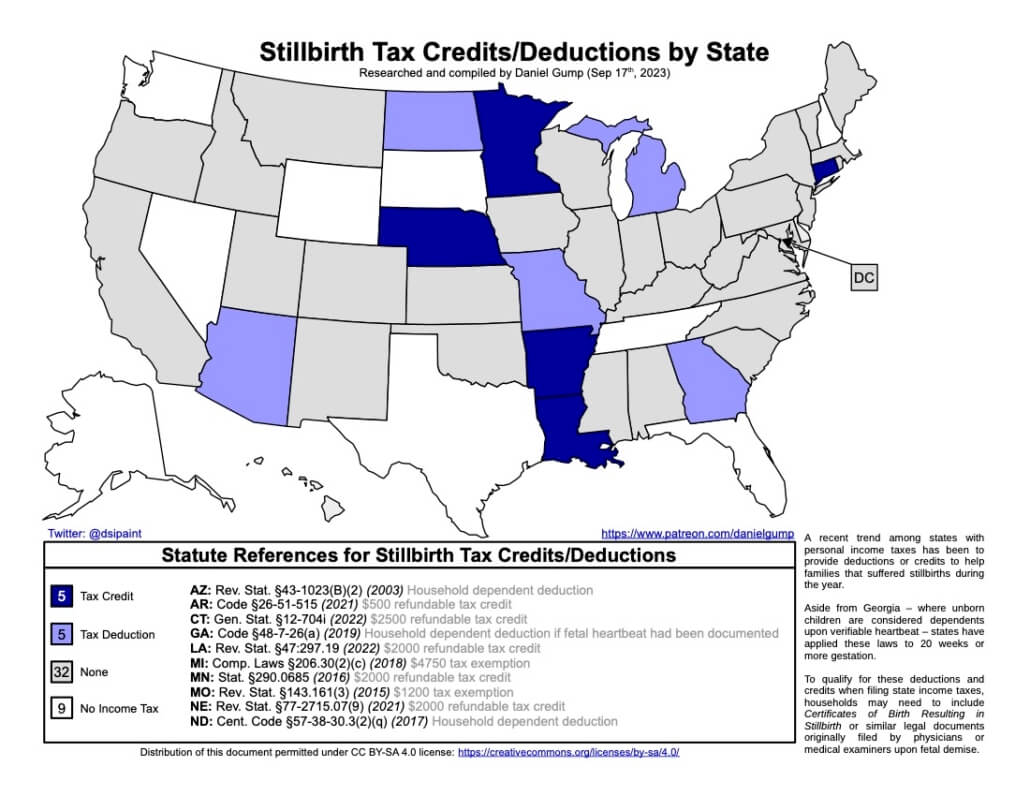

After the Supreme Court’s Dobbs ruling in 2022, the Georgia Department of Revenue issuing guidance on filing. Though nine other states offer tax credits or tax deductions upon stillbirth, Georgia has stood alone in being the only state for which an unborn child is a tax dependent during an ongoing pregnancy. This may soon change with the introduction of House Bill 87 in Ohio.

The STORK Act

Ohio’s House Bill 87, to be known as the Strategic Tax Opportunities for Raising Kids (STORK) Act, contains several provisions:

- Sec. 5739.02 (pp. 31-32): Tax incentives for several additional infant care items (e.g. clothing, pacifiers, cribs, breast pumps, baby monitors, toys, etc.)

- Sec. 5747.01 (pp. 57-58): Expand the state income tax definition of “dependent” to include unborn children

- Sec. 5747.01 (p. 63): Small grammatical correction (“were” -> “was”)

- Sec. 5747.025 (pp. 73-74): For separate tax filings, only the “expecting mother” can claim the dependency

- The changes would affect tax year 2026.

Here is the raw text for the second point that would be added to the Revised Code:

“Dependents” shall include each child conceived, including each child conceived by assisted reproduction that has been placed inside the taxpayer or taxpayer’s spouse’s uterus or lost to spontaneous miscarriage, by the taxpayer or the taxpayer’s spouse during the taxable year, so long as:

(a) The child is not also a qualifying child, as that term is defined in section 152 of the Internal Revenue Code, for the same taxable year.

(b) The child’s life was not terminated in an abortion, including by selective reduction.

As used in division (O) of this section, “assisted reproduction” has the same meaning as in section 2907.13 of the Revised Code and “spontaneous miscarriage” has the same meaning as in section 2919.19 of the Revised Code.

Similarly to Georgia, Ohio would allow for the unborn child’s dependency to still count on the tax filing upon “spontaneous miscarriage” (including stillbirth).

Opposition to the Bill

Since the bill explicitly excludes the tax dependency when the unborn child’s life is ended by induced abortion, it has already met opposition by the Ohio abortion activist group Abortion Forward. They claim the following:

It is clear what the sponsors are doing with this bill: turning pregnant people into simple vessels whose only role is to carry a pregnancy and whose rights are superseded by newly created rights for fetuses and embryos from the moment of conception.

The statement by Abortion Forward does not proceed to explain how they have reached this conclusion. However, one could argue that they have the logic in reverse, as striking the induced abortion exception from the text could allow for abusers and sex traffickers to further profit from their victims by forcing pregnancy then inducing abortion. This would be “turning pregnant people into simple vessels whose only role is to carry a pregnancy.”

History of Similar Legislation

The push for including unborn children as tax dependents is not new in Ohio. The first such attempt came in summer of 2022, and I was actually the one to do so. Within a few weeks of Dobbs ruling in June 2022, I personally met with my own first-term state representative to present a bill I drafted to address several items in the state relating to childcare. None of these items related to induced abortions, and my representative deemed none of them particularly controversial in the 2022 political climate.

Provisions included the following:

- Allow for termination of parental rights by a civil standard to a child conceived in rape or sexual battery

- Allow for 501(c)(3) charitable organizations to submit prenatal support expenses to paternity court for reimbursement

- Expand prenatal aspects of child support from applying to just “pregnancy and confinement” (in place for a century in Ohio) to also covering the mother’s health insurance premiums during pregnancy and her lost wages due to medical necessity

- Extend the deadline for genetic testing in paternity proceedings from forty-five days to “as early as safely possible beyond forty-five days for an unborn child.”

- Add rape and sexual battery to crimes for which names should be concealed on administrative orders regarding parent and child relationships

- Expand the definition of “Dependents” for state taxes to also include “any unborn child with a detectable heartbeat… even if the pregnancy ends in miscarriage or stillbirth.”

For that final point, I also sought to amend O.R.C. 5747.01 (to same section to be amended in HB 87), adapting text from Georgia:

(1) For taxable years beginning on or after January 1, 2023, dependents as defined in the Internal Revenue Code, provided, however, that any unborn child with a detectable heartbeat shall qualify as a dependent minor, even if the pregnancy ends in miscarriage or stillbirth;

This proposal went nowhere through the end of the 134th General Assembly’s regular session, when O.R.C. 2919.195 still banned induced abortions after the detectable heartbeat. No bills relating to topics within the proposal saw introduction during the 135th General Assembly, when a ballot initiative for the Ohio Constitution added the “Right to Reproductive Freedom” in Art. 1, Sec. 22, to enshrine the legal right to induced abortions. Finally, HB 87 has come during the 136th General Assembly session.

As a loss-parent, I hope to see this 2026 legislation pass to provide assistance to parents who face medical bills during both successful pregnancies and when they experience tragic losses of their unborn children. It frustrates me that an organization would to frame this bill negatively, when it simply aims to help parents at the time when they need it the most.

If you appreciate our work and would like to help, one of the most effective ways to do so is to become a monthly donor. You can also give a one time donation here or volunteer with us here.